We use strictly necessary cookies to enable our site to work and performance cookies to improve the visitor experience when visiting the site. We will only set performance cookies if you permit us to.

For more detailed information about the cookies we use, see the „Cookie Usage“ section of our Privacy Policy

Wandelanleihen bieten eine hybride Lösung für Anleger, die ein ausgewogenes Engagement am Finanzmarkt wünschen, welches die Vorteile von Aktien und Anleihen kombiniert. Seit mehr als einem Jahrzehnt verwendet unser Team proprietäre Modelle und Systeme, um die attraktivsten Chancen innerhalb dieser Anlageklasse zu identifizieren. Wir bieten eine Auswahl an aktiv verwalteten Lösungen, welche darauf ausgelegt sind, das attraktive, asymmetrische Renditeprofil von Wandelanleihen mit unterschiedlichen Risikotoleranzen zu nutzen.

Wir investieren in eine kleine Auswahl hochwertiger europäischer Unternehmen, bei denen wir durch die Lösung bestimmter unternehmensspezifischer Probleme potenziell bedeutende Möglichkeiten zur Schaffung von Mehrwert erkennen. Wir wirken als Katalysator für Veränderungen, indem wir konstruktiv mit den Unternehmen und mit anderen Aktionären zusammenarbeiten.

Ein sehr erfahrenes Team mit einer nachgewiesenen Erfolgsbilanz bei der Erzielung positiver Ergebnisse für Anleger. Die bewährte Anlagemethode, die Dividendenkraft der Titel voll auszuschöpfen, bietet das Potential, langfristig mehr Rendite bei unterdurchschnittlichen Volatilitätsraten einzufahren. Das Team ist sucht gezielt nach der seltenen Kombination aus hohen Renditen, nachhaltigen Dividenden und einer attraktiven Bewertung, welche nur dann auftritt, wenn es gewisse Kontroversen gibt. Indem wir alles daran setzen, diese Kontroveren im Kern zu verstehen, erhöhen wir für Sie aktiv die Wahrscheinlichkeit eines Investitionserfolges.

Japan ist die drittgrösste Volkswirtschaft der Welt. Die Unternehmenslandschaft des Landes befindet sich seit einigen Jahren im Umbruch. Durch unser Joint Venture mit dem in Tokio ansässigen Nissay Asset Management (NAM) investieren wir in eine kleine Anzahl ausgewählter japanischer Unternehmen, deren Bewertung aufgrund von Faktoren, welche wir für korrigierbar halten, nicht ihr volles Potenzial widerspiegelt. Wir agieren für diese Unternehmen als Partner im Change-Prozess, damit der Wandel, der zur Freisetzung des Potenzials notwendig ist, vollzogen werden kann.

Unser Nachhaltigkeitsansatz bei der Anlagetätigkeit beruht auf drei Säulen: einer soliden Unternehmensführung und einem strengen Richtlinien Regelwerk für alle Redwheel-Fonds, einer zentralisierten Stewardship-Expertise für unsere Anlageteams, von denen jedes sein eigenes individuelles Engagement für die Unternehmen, in die es investiert, durchführt, und Greenwheel, unserem hauseigenen Team von Experten für Nachhaltigkeitsresearch.

Die Abteilung ‚Stewardship and Regulatory Change‘ von Redwheel ist für die operative Unterstützung des Stewardship bei Redwheel zuständig.

Das Team für Nachhaltigkeitsstrategie, Governance und Richtlinien berät und unterstützt Redwheel und seine Anlageteams bei der Integration von Nachhaltigkeitsaspekten in die Anlageprozesse und trägt dazu bei, dass sich Redwheel‘s Ansatz für verantwortungsbewusste Anlagen im Einklang mit den Kundenbedürfnissen und regulatorischen Anforderungen weiterentwickelt.

Greenwheel ist der Partner für die Nachhaltigkeitsanalysen der Redwheel-Fonds ‘Sustainable, Transition und Enhanced Integration’. Greenwheel bietet Redwheel-Fondsmanagern in jeder Phase des Lebenszyklus nachhaltiger Produkte maßgeschneidertes Nachhaltigkeits-Research und Beratung auf thematischer und sektoraler Ebene, von der Fondsgestaltung bis hin zu Investment-Research und Engagement-Unterstützung, abhängig von den Bedürfnissen und Anforderungen des jeweiligen Teams. Das von den Fondsmanagern in Auftrag gegebene Modell gewährleistet, dass das Research auf das Anlageprodukt und das Kundenergebnis zugeschnitten ist

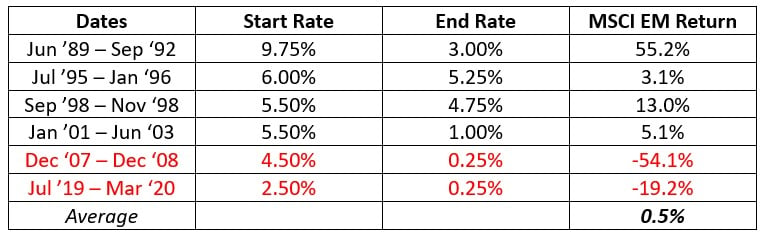

There have been six cycles of monetary easing by the US Federal Reserve since the inception of the MSCI Emerging Markets Index in January 1988. Conventional wisdom presumes that lower interest rates reduce the attraction of cash and bonds in relation to riskier assets with growth characteristics, including emerging markets (EM) equities, and this has been true more often than not.

Source: Bloomberg, Redwheel as of 31 August 2024. Past performance is not a guide to future results.

The equity market outcome depends on the reason for rate cuts

Although the average gain is only 0.5%, the MSCI Emerging Markets Index rose on 4 out of 6 occasions. Where the Federal Reserve has successfully engineered a soft landing (early and mid-90s) or averted an economic or financial crisis (1998 Russian default and early-2000s ‘Tech Wreck’), the average gain during the period of lowering rates has been just over 19%. On the other hand, a rearguard action in response to a sudden global shock (2008 Global Financial Crisis and 2020 COVID-19 pandemic) coincided with average losses of over 36%.

Source: Bloomberg, Redwheel as of 31 August 2024. Past performance is not a guide to future results.

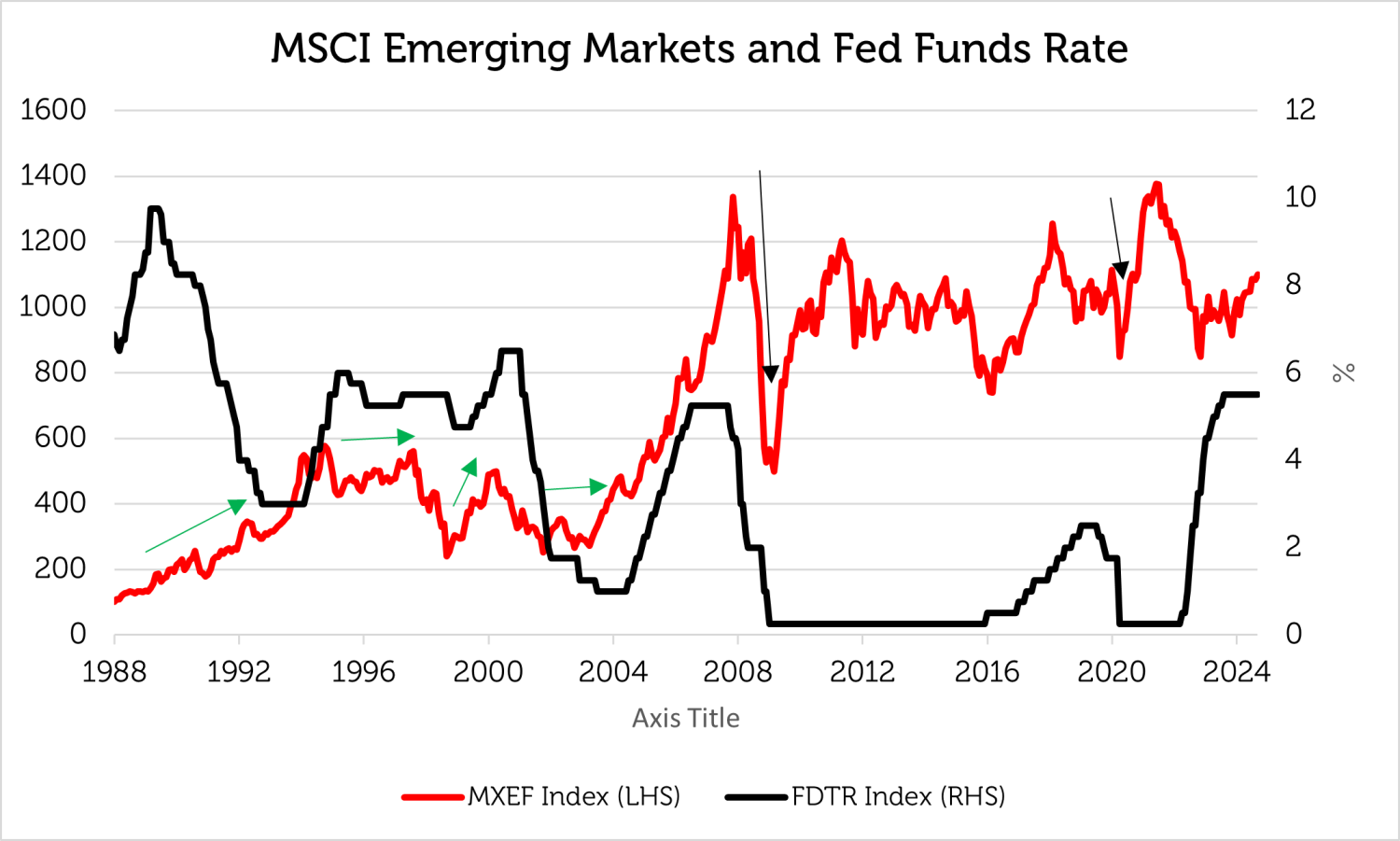

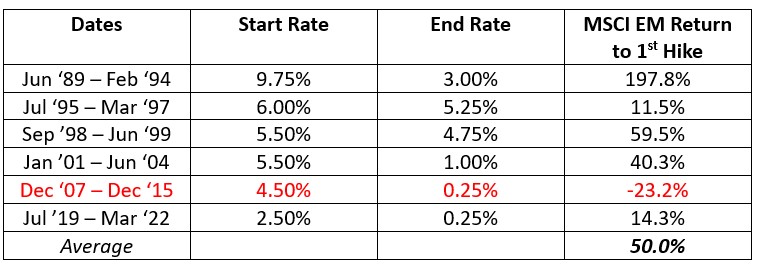

It’s better at the bottom of the rate cycle

Although EM equity performance has generally been positive during the period of interest rate reductions, it has been typically better from the time when the Federal Reserve finishes cutting rates to the first increase of the next cycle. The period between the first interest rate reduction and the first increase in the subsequent rate cycle has historically been beneficial for equity markets, delivering an average return of 50%. This reflects that improvement in growth that lower interest rates eventually deliver. The only exception was the Global Financial Crisis and its aftermath, when even an extended period of Zero Interest Rate Policy (ZIRP) could not propel the MSCI Emerging Markets Index beyond the Super-Cycle high that was reached in 2007. The features of the Global Financial Crisis were not only the depth of the bear market, but the unusually high valuations that Emerging Markets had reached, which had to normalize during the period of ZIRP.

Source: Bloomberg, Redwheel as of 31 August 2024. Past performance is not a guide to future results.

Where are we now?

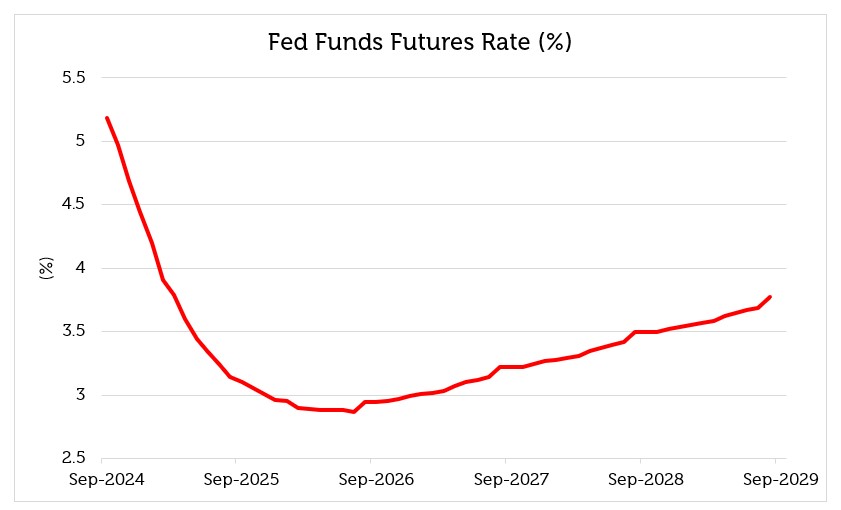

We believe that the Federal Reserve is in the process of engineering a soft landing such that the gradual reduction in interest rates will avert a recession. The Fed Funds Rate should fall from its current range of 5.25% – 5.50% today to 2.75% – 3.00% by the end of 2025. This would be in line with average Federal Reserve easing since 1989: a 2.50% reduction in the overnight rate over a sixteen-month period.

Source: Bloomberg, Redwheel as of 31 August 2024. Past performance is not a guide to future results.

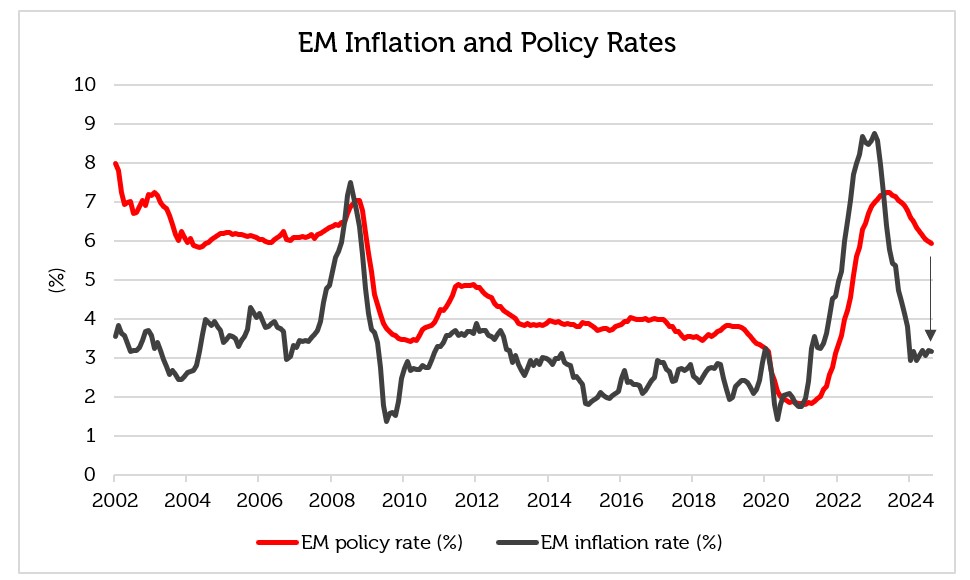

This would allow emerging market central banks to reduce their own overnight interest rates, which is justified by the deceleration in local inflation, but which has been delayed by the long plateau of high rates in the US. Many Emerging Market central banks worry about the potential for currency weakness if they pre-empt the Federal Reserve in lowering rates.

Source: HSBC, Redwheel as of 31 August 2024. Past performance is not a guide to future results.

The effects of rate cuts in EM

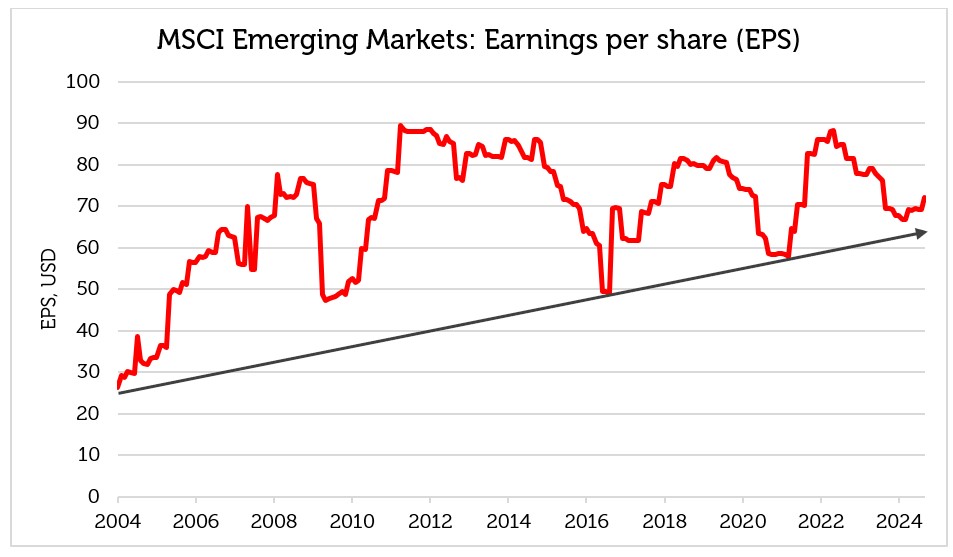

Lower interest rates have the potential to help emerging markets equities in two ways. First, easier monetary policy can stimulate economic activity by lowering corporate and household interest expenses and freeing up money for consumption and investment. Accelerating economic growth should feed into higher corporate earnings, which are close to a cyclical trough and starting to recover.

Source: Bloomberg, Redwheel as of 31 August 2024. Past performance is not a guide to future results.

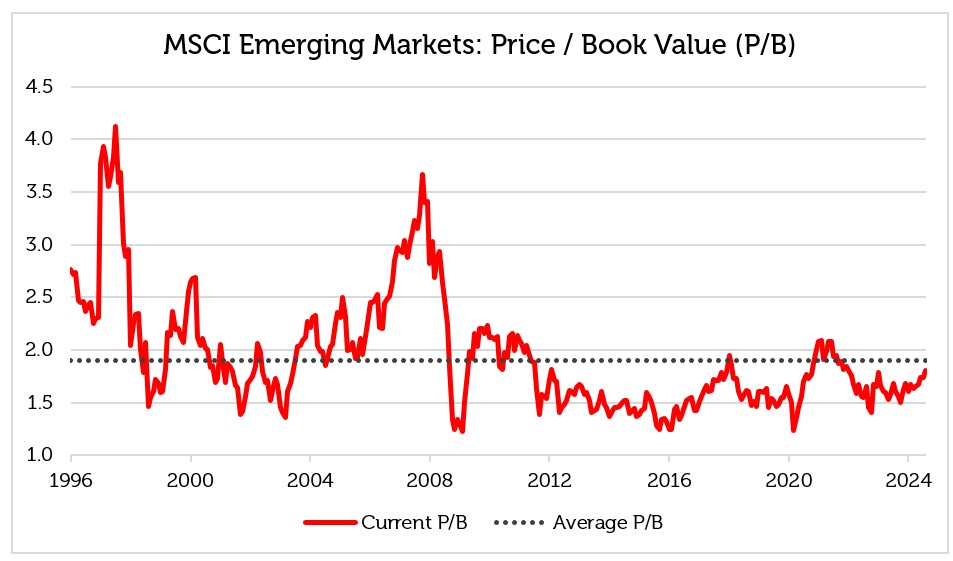

Second, the combination of lower rates and higher earnings should cause an upward re-rating of equities, because higher growth should be discounted at a lower rate, leading to higher valuations. The current Price to Book Value ratio of 1.7 is slightly below its long run average of 1.9, suggesting there is more potential for upside than downside at this level.

Source: Bloomberg, Redwheel as of 31 August 2024. Past performance is not a guide to future results.

Key Information

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Past performance is not a guide to future results. The prices of investments and income from them may fall as well as rise and an investor’s investment is subject to potential loss, in whole or in part. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so. The statements and opinions expressed in this article are those of the author as of the date of publication, and do not necessarily represent the view of Redwheel. This article does not constitute investment advice and the information shown is for illustrative purposes only.

Health care earnings forecasts are almost on a par with tech, yet the sector trades at a compelling discount. New research from Redwheel’s Life Changing Treatments team reveals that health care offers tech-like earnings growth potential yet trades at a historic 50% valuation discount as a more favourable political backdrop and robust innovation continues to drive the sector forward.

Healthcare valuations are at their lowest since the financial crisis, yet fundamentals are solid. Can we expect a rerating?

Imagine companies were money-printing machines in a shop. How would we value each machine and what would we make of constantly shifting prices? Learn how investors can reframe their perspective of extreme market conditions.

Redwheel ® and Ecofin ® are registered trademarks of RWC Partners Limited (“RWC”). The term “Redwheel” may include any one or more Redwheel branded regulated entities including RWC Asset Management LLP, which is authorised and regulated by the UK Financial Conduct Authority and the US Securities and Exchange Commission (“SEC”); RWC Asset Advisors (US) LLC, which is registered with the SEC; RWC Singapore (Pte) Limited, which is licensed as a Licensed Fund Management Company by the Monetary Authority of Singapore; Redwheel Australia Pty Ltd is an Australian Financial Services Licensee with the Australian Securities and Investment Commission; and Redwheel Europe Fondsmæglerselskab A/S which is regulated by the Danish Financial Supervisory Authority.

Redwheel may act as investment manager or adviser, or otherwise provide services, to more than one product pursuing a similar investment strategy or focus to the product detailed in this document. Redwheel and RWC (together “Redwheel Group”) seeks to minimise any conflicts of interest, and endeavours to act at all times in accordance with its legal and regulatory obligations as well as its own policies and codes of conduct.

This document is directed only at professional, institutional, wholesale or qualified investors. The services provided by Redwheel are available only to such persons. It is not intended for distribution to and should not be relied on by any person who would qualify as a retail or individual investor in any jurisdiction or for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to local law or regulation.

This document has been prepared for general information purposes only and has not been delivered for registration in any jurisdiction nor has its content been reviewed or approved by any regulatory authority in any jurisdiction.

The information contained herein does not constitute: (i) a binding legal agreement; (ii) legal, regulatory, tax, accounting or other advice; (iii) an offer, recommendation or solicitation to buy or sell shares in any fund, security, commodity, financial instrument or derivative linked to, or otherwise included in a portfolio managed or advised by Redwheel; or (iv) an offer to enter into any other transaction whatsoever (each a “Transaction”). Redwheel Group bears no responsibility for your investment research and/or investment decisions and you should consult your own lawyer, accountant, tax adviser or other professional adviser before entering into any Transaction. No representations and/or warranties are made that the information contained herein is either up to date and/or accurate and is not intended to be used or relied upon by any counterparty, investor or any other third party.

Redwheel Group uses information from third party vendors, such as statistical and other data, that it believes to be reliable. However, the accuracy of this data, which may be used to calculate results or otherwise compile data that finds its way over time into Redwheel Group research data stored on its systems, is not guaranteed. If such information is not accurate, some of the conclusions reached or statements made may be adversely affected. Any opinion expressed herein, which may be subjective in nature, may not be shared by all directors, officers, employees, or representatives of Group and may be subject to change without notice. Redwheel Group is not liable for any decisions made or actions or inactions taken by you or others based on the contents of this document and neither Redwheel Group nor any of its directors, officers, employees, or representatives (including affiliates) accepts any liability whatsoever for any errors and/or omissions or for any direct, indirect, special, incidental, or consequential loss, damages, or expenses of any kind howsoever arising from the use of, or reliance on, any information contained herein.

Information contained in this document should not be viewed as indicative of future results. Past performance of any Transaction is not indicative of future results. The value of investments can go down as well as up. Certain assumptions and forward looking statements may have been made either for modelling purposes, to simplify the presentation and/or calculation of any projections or estimates contained herein and Redwheel Group does not represent that that any such assumptions or statements will reflect actual future events or that all assumptions have been considered or stated. There can be no assurance that estimated returns or projections will be realised or that actual returns or performance results will not materially differ from those estimated herein. Some of the information contained in this document may be aggregated data of Transactions executed by Redwheel that has been compiled so as not to identify the underlying Transactions of any particular customer.

No representations or warranties of any kind are intended or should be inferred with respect to the economic return from, or the tax consequences of, an investment in a Redwheel-managed fund.

This document expresses no views as to the suitability or appropriateness of the fund or any other investments described herein to the individual circumstances of any recipient.

The information transmitted is intended only for the person or entity to which it has been given and may contain confidential and/or privileged material. In accepting receipt of the information transmitted you agree that you and/or your affiliates, partners, directors, officers and employees, as applicable, will keep all information strictly confidential. Any review, retransmission, dissemination or other use of, or taking of any action in reliance upon, this information is prohibited. Any distribution or reproduction of this document is not authorised and is prohibited without the express written consent of Redwheel Group.

Funds managed by Redwheel are not, and will not be, registered under the Securities Act of 1933 (the “Securities Act”) and are not available for purchase by US persons (as defined in Regulation S under the Securities Act) except to persons who are “qualified purchasers” (as defined in the Investment Company Act of 1940) and “accredited investors” (as defined in Rule 501(a) under the Securities Act).

This document does not constitute an offer to sell, purchase, subscribe for or otherwise invest in units or shares of any fund managed by Redwheel. Any offering is made only pursuant to the relevant offering document and the relevant subscription application. Prospective investors should review the offering memorandum in its entirety, including the risk factors in the offering memorandum, before making a decision to invest.

AIFMD and Distribution in the European Economic Area (“EEA”)

The Alternative Fund Managers Directive (Directive 2011/61/EU) (“AIFMD”) is a regulatory regime which came into full effect in the EEA on 22 July 2014. RWC Asset Management LLP is an Alternative Investment Fund Manager (an “AIFM”) to certain funds managed by it (each an “AIF”). The AIFM is required to make available to investors certain prescribed information prior to their investment in an AIF. The majority of the prescribed information is contained in the latest Offering Document of the AIF. The remainder of the prescribed information is contained in the relevant AIF’s annual report and accounts. All of the information is provided in accordance with the AIFMD.

In relation to each member state of the EEA (each a “Member State”), this document may only be distributed and shares in a Redwheel fund (“Shares”) may only be offered and placed to the extent that (a) the relevant Redwheel fund is permitted to be marketed to professional investors in accordance with the AIFMD (as implemented into the local law/regulation of the relevant Member State); or (b) this document may otherwise be lawfully distributed and the Shares may lawfully be offered or placed in that Member State (including at the initiative of the investor).

Information Required for Offering in Switzerland of Foreign Collective Investment Schemes to Qualified Investors within the meaning of Article 10 CISA.

This is an advertising document.

The representative and paying agent of the Redwheel-managed funds in Switzerland (the “Representative in Switzerland”) FIRST INDEPENDENT FUND SERVICES LTD, Feldeggstrasse 12, CH-8008 Zurich. Swiss Paying Agent: Helvetische Bank AG, Seefeldstrasse 215, CH-8008 Zurich. In respect of the units of the Redwheel-managed funds offered in Switzerland, the place of performance is at the registered office of the Swiss Representative. The place of jurisdiction is at the registered office of the Swiss Representative or at the registered office or place of residence of the investor.

Redwheel ® ist eine eingetragene Marke von RWC Partners Limited. Der Begriff Redwheel kann ein oder mehrere von Redwheel beaufsichtigte Unternehmen umfassen, einschliesslich der RWC Asset Management LLP, die von der Financial Conduct Authority im Vereinigten Königreich zugelassen ist und beaufsichtigt wird („RWC“). RWC ist eine in England und Wales eingetragene Gesellschaft mit Sitz in Verde 4th Floor, 10 Bressenden Place, London, SW1E 5DH, Vereinigtes Königreich, und der eingetragenen Nummer OC332015.

Wir verwenden ausschliesslich erforderliche Cookies, damit unsere Website funktioniert, und Leistungscookies, um das Besuchererlebnis beim Besuch der Website zu verbessern. Wir nutzen Performance-Cookies nur, wenn Sie uns dies erlauben.

Ausführlichere Informationen zu den von uns verwendeten Cookies finden Sie im Abschnitt „Cookie-Nutzung“ unserer Datenschutzerklärung

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment.The term “RWC” may include any one or more RWC branded entities including RWC Partners Limited and RWC Asset Management LLP, each of which is authorised and regulated by the UK Financial Conduct Authority and, in the case of RWC Asset Management LLP, the US Securities and Exchange Commission; RWC Asset Advisors (US) LLC, which is registered with the US Securities and Exchange Commission; and RWC Singapore (Pte) Limited, which is licensed as a Licensed Fund Management Company by the Monetary Authority of Singapore.RWC may act as investment manager or adviser, or otherwise provide services, to more than one product pursuing a similar investment strategy or focus to the product detailed in this audio. RWC seeks to minimise any conflicts of interest, and endeavours to act at all times in accordance with its legal and regulatory obligations as well as its own policies and codes of conduct.This audio is directed only at professional, institutional, wholesale or qualified investors. The services provided by RWC are available only to such persons. It is not intended for distribution to and should not be relied on by any person who would qualify as a retail or individual investor in any jurisdiction or for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to local law or regulation.This audio has been prepared for general information purposes only and has not been delivered for registration in any jurisdiction nor has its content been reviewed or approved by any regulatory authority in any jurisdiction. The information contained herein does not constitute: (i) a binding legal agreement; (ii) legal, regulatory, tax, accounting or other advice; (iii) an offer, recommendation or solicitation to buy or sell shares in any fund, security, commodity, financial instrument or derivative linked to, or otherwise included in a portfolio managed or advised by RWC; or(iv) an offer to enter into any other transaction whatsoever (each a “Transaction”). No representations and/or warranties are made that the information contained herein is either up to date and/or accurate and is not intended to be used or relied upon by any counterparty, investor or any other third party.RWC uses information from third party vendors, such as statistical and other data, that it believes to be reliable. However, the accuracy of this data, which may be used to calculate results or otherwise compile data that finds its way over time into RWC research data stored on its systems, is not guaranteed. If such information is not accurate, some of the conclusions reached or statements made may be adversely affected. RWC bears no responsibility for your investment research and/or investment decisions and you should consult your own lawyer, accountant, tax adviser or other professional adviser before entering into any Transaction. Any opinion expressed herein, which may be subjective in nature, may not be shared by all directors, officers, employees, or representatives of RWC and may be subject to change without notice. RWC is not liable for any decisions made or actions or in actions taken by you or others based on the contents of this audio and neither RWC nor any of its directors, officers, employees, or representatives (including affiliates) accepts any liability whatsoever for any errors and/or omissions or for any direct, indirect, special, incidental, or consequential loss, damages, or expenses of any kind howsoever arising from the use of, or reliance on, any information contained herein.Information contained in this audio should not be viewed as indicative of future results. Past performance of any Transaction is not indicative of future results. The value of investments can go down as well as up. Certain assumptions and forward looking statements may have been made either for modelling purposes, to simplify the audio and/or calculation of any projections or estimates contained herein and RWC does not represent that that any such assumptions or statements will reflect actual future events or that all assumptions have been considered or stated. Forward-looking statements are inherently uncertain, and changing factors such as those affecting the markets generally, or those affecting particular industries or issuers, may cause results to differ from those discussed. Accordingly, there can be no assurance that estimated returns or projections will be realised or that actual returns or performance results will not materially differ from those estimated herein. Some of the information contained in this audio may be aggregated data of Transactions executed by RWC that has been compiled so as not to identify the underlying Transactions of any particular customer.The information transmitted is intended only for the person or entity to which it has been given and may contain confidential and/or privileged material. In accepting receipt of the information transmitted you agree that you and/or your affiliates, partners, directors, officers and employees, as applicable, will keep all information strictly confidential. Any review, retransmission, dissemination or other use of, or taking of any action in reliance upon, this information is prohibited. The information contained herein is confidential and is intended for the exclusive use of the intended recipient(s) to which this audio has been provided. Any distribution or reproduction of this audio is not authorised and is prohibited without the express written consent of RWC or any of its affiliates.Changes in rates of exchange may cause the value of such investments to fluctuate. An investor may not be able to get back the amount invested and the loss on realisation may be very high and could result in a substantial or complete loss of the investment. In addition, an investor who realises their investment in a RWC-managed fund after a short period may not realise the amount originally invested as a result of charges made on the issue and/or redemption of such investment. The value of such interests for the purposes of purchases may differ from their value for the purpose of redemptions. No representations or warranties of any kind are intended or should be inferred with respect to the economic return from, or the tax consequences of, an investment in a RWC-managed fund. Current tax levels and reliefs may change. Depending on individual circumstances, this may affect investment returns. Nothing in this document constitutes advice on the merits of buying or selling a particular investment. This audio expresses no views as to the suitability or appropriateness of the fund or any other investments described herein to the individual circumstances of any recipient.AIFMD and Distribution in the European Economic Area (“EEA”)The Alternative Fund Managers Directive (Directive 2011/61/EU)(“AIFMD”) is a regulatory regime which came into full effect in the EEA on 22 July 2014. RWC Asset Management LLP is an Alternative Investment Fund Manager (an “AIFM”) to certain funds managed by it (each an “AIF”). The AIFM is required to make available to investors certain prescribed information prior to their investment in an AIF. The majority of the prescribed information is contained in the latest Offering Document of the AIF. The remainder of the prescribed information is contained in the relevant AIF’s annual report and accounts. All of the information is provided in accordance with the AIFMD.In relation to each member state of the EEA (each a “Member State”),this document may only be distributed and shares in a RWC fund(“Shares”) may only be offered and placed to the extent that (a) the relevant RWC fund is permitted to be marketed to professional investors in accordance with the AIFMD (as implemented into the local law/regulation of the relevant Member State); or (b) this audio may otherwise be lawfully distributed and the Shares may lawfully offered or placed in that Member State (including at the initiative of the investor).Information Required for Distribution of Foreign Collective Investment Schemes to Qualified Investors in SwitzerlandThe representative and paying agent of the RWC-managed funds in Switzerland (the “Representative in Switzerland”) FIRST INDEPENDENT FUND SERVICES LTD, Klausstrasse 33, CH-8008 Zurich. Swiss Paying Agent: Helvetische Bank AG, Seefeldstrasse 215, CH-8008 Zurich. In respect of the units of the RWC-managed funds distributed in Switzerland, the place of performance and jurisdiction is at the registered office of the Representative in Switzerland.