Mr Market’s reaction to news can oscillate wildly, which is why it is important to remember to follow a process and not let emotions drive decision making.

A case in point is Tapestry, the parent company of the Coach and Kate Spade fashion brands.

When we invested in Tapestry our investment thesis centred around the majority of the business (Coach) continuing to trade well, whilst the smaller part (Kate Spade – around 20%) needed turning around. This put the idea firmly in our ‘Profit Transformation’ bucket, with a valuation that did not expect this turnaround to happen any time soon, and a decent balance sheet that made the investment attractive from a risk/reward perspective in our view, when the range of potential outcomes were considered.

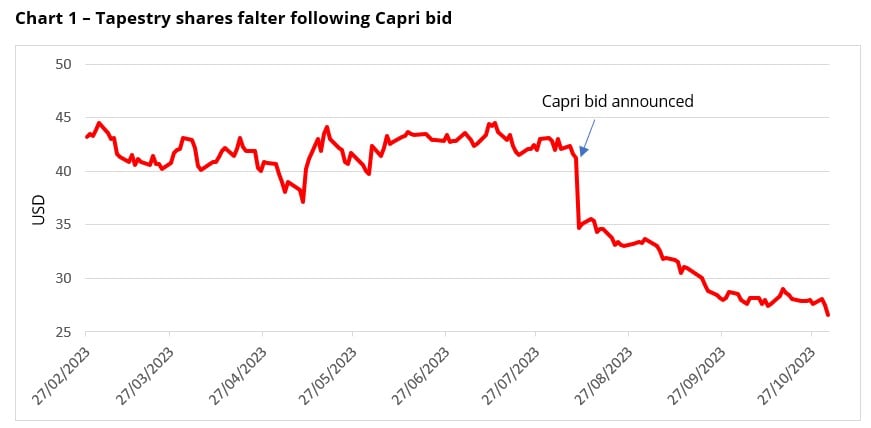

Then, on 10 August 2023, Tapestry announced its intention to buy Capri Holdings, parent company of Michael Kors, Versace, and Jimmy Choo. The mooted deal involves Tapestry paying $57 per share in cash (read: ‘debt for Tapestry shareholders ’). This led to a collapse in the share price of c.16% on the day, followed by a further fall of c.23% resulting in a total decline of c.35% in reaction to the announcement (See Bloomberg chart below).[1]

Source: Bloomberg as at 1st November 2023. The information shown above is for illustrative purposes. Past performance is not a guide to future results.

Over this time emotions kick in, none of them joyous! The investment thesis was to be turned on its head, yet it was important to apply the process and not let emotions govern our response.

In other words, apply our process to Capri, to understand the probability and range of outcomes for the new combined group. The result of this was a fan of outcomes that showed a meaningful shift in the risk reward of the Investment thesis. The company changes from originally 20% of the business needing turning around to comfortably over 50%, with the need to improve all three of Capri’s brands – Michael Kors, Versace and Jimmy Choo. Although the turnaround of these brands is a well-trodden path of reducing the dependence upon wholesale channels and instead selling direct to consumers; the scale of change is from our point of view greater than normal, with for example c.30% of Michael Kors sales currently still wholesale (having been c.50% 10 years ago). For reference, best-in-class aspirational brands have c.10% of sales via wholesale.[2]

Our lessons learnt from previous investments teach that the presence of debt usually removes the luxury of time for a company. This deal could raise Tapestry’s debt to c.5x EBITDA, meaning that not only are they taking on a large turnaround, representing the majority of the business; they will also have to be successful quickly because of the need to reduce the debt. This further increases the risk.[3]

The second lesson learnt is that increased debt can hurt a company’s ability to sustain a dividend through difficult periods if anything goes wrong. In this scenario, it becomes increasingly likely a company is forced to cut the dividend to appease debt holders. This further increases the risk again.

Finally, another lesson learnt is that the longer it takes to complete the deal, the greater the probability that the assets acquired are worse off than first thought. The deal for Capri is on track to take almost a year to close. Further increase in risk again.

Thus, we believe the valuation of the potential combined group has shifted to less favourable.

However, until the deal completes, a window opened up whereby Coach (and Kate Spade) as stand-alone businesses were trading far cheaper than before the share price fall. This introduced the risk of a counter bid – if anyone desired Coach as a brand this was the time to act.

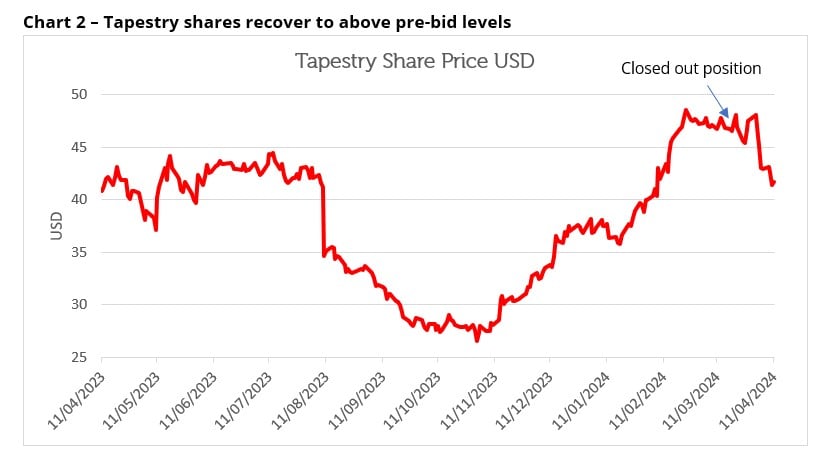

And then Mr Market changed his response completely, to march the shares up around 82% from the 1 November low to the 28 February 2024 high – higher than before the bid announcement! (See Bloomberg chart below).[4]

Source: Bloomberg, at 11 April 2024 . The information shown above is for illustrative purposes. Past performance is not a guide to future results.

What has actually changed to justify this recovery? There is little evidence to suggest the deal is not still to happen. Certainly, Tapestry has continued to report good numbers, but Capri certainly hasn’t. So, does this create a great opportunity, the worst Capri trades, the greater the turnaround potential? Emotions change, largely influenced by the behaviour of the share price! Long gone is the misery of November.

The discipline of our process again helps to protect us against the wider emotion of the market. We believe the recovery in the Tapestry share price has only made the risk and reward ratio further skewed against investors and removed the counter bid risk.

So even though Mr Market’s emotions have changed as quickly as tastes in fashion, and now believes the Jimmy Choos will fit just perfect, our disciplines not emotions have led us to ditch the Choos and exit Tapestry.

Sources:

[1] Bloomberg as at 1st November 2023

[2] Capri company report and accounts, 31st December 2023

[3]Redwheel as at 25.03.24

[4] Bloomberg as at 25.03.24

Key Information

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Past performance is not a guide to future results. The prices of investments and income from them may fall as well as rise and an investor’s investment is subject to potential loss, in whole or in part. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so. The statements and opinions expressed in this article are those of the author as of the date of publication, and do not necessarily represent the view of Redwheel. This article does not constitute investment advice and the information shown is for illustrative purposes only.