In May 2020, we wrote a blog entitled ‘In for free’ in which we looked at a group of stocks which were so cheap that we felt one division was worth more than the value of the entire group and hence the remaining parts of the business were essentially ‘in for free’.

‘Some of our most successful investments have been ones in which sentiment towards a company becomes so negative, that the valuation ends up making no sense versus the worth of its various parts. Sometimes this is so extreme that you can buy a business where one part of it is worth more than the valuation of the entire group and so in effect, you are getting the other parts ‘for free’.

In yet another example of how irrational the valuations of companies suffering temporary earnings declines have become, we believe the market today is offering a number of opportunities to buy companies where you are getting part of it for nothing.’

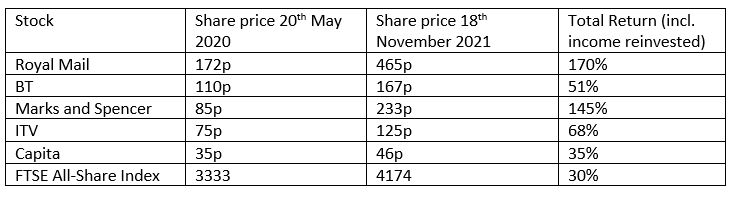

We thought that it would be worthwhile seeing how these companies had performed since then and the updated results are shown below. On the face of it, the gains would seem to suggest that there is some merit to buying stocks at such a discount that one part represents more than the entire group.

Past performance is not a guide to the future. The price of investments and the income from them may fall as well as rise and investors may not get back the full amount invested.

The information shown above is for illustrative purposes only and is not intended to be, and should not be interpreted as, recommendations or advice.

When share prices rise by as much as some of those shown above, it is tempting to conclude that they must now be fairly valued or even expensive but of course this fails to account for both how extreme the starting levels of undervaluation were as well as the fact that the operating performance of some of these businesses has improved dramatically over the period. The two examples below hopefully demonstrate this.

- Royal Mail

Our argument in our original note was that the European parcels business (known as GLS) was worth £2bn and given that the entire group was valued at £1.7bn, the UK business was being ascribed a negative value. Royal Mail now believes that the GLS business will make €500m of operating profits in 2023/24 (Bloomberg Consensus Estimates) which if we value at 10x gives €5bn or £4.3bn. Coincidentally, this is the market cap of the entire group suggesting the market is still ascribing no value to the UK business despite the rise in the share price in the past year. This is now even more puzzling given the improvement in the outlook for the UK business which also has 50% market share in UK parcels.

- Marks and Spencer

Our thesis for Marks was that the market was ascribing no value to its clothing and home business, if one put a reasonable value on its food retail operation and its stake in Ocado. Since our original blog, the share price has risen by 145% and whilst the market has belatedly begun to recognise the transformation going on within the company, we would still argue that the market is not ascribing full value to the assets. The current enterprise value of Marks is £5.6bn or £4.1bn once we deduct the value of their stake in Ocado which we estimate at £1.5bn. The Marks & Spencer food business is forecast to make about £280m of operating profit (Bloomberg Consensus Estimates) this year which if valued on a post-tax p/e of 13x would be worth £2.9bn, whilst their International business could be worth £1.1bn. Deducting these we can estimate that the Clothing and Home business is being valued by the stock market at c. £100m despite the fact that Marks is the UK’s number one clothing retailer by market share (number two on line) and is forecast to make operating profits of over £300m this year (Bloomberg Consensus Estimates) . In addition, it is worth considering that Marks owns a significant amount of the real estate from which it operates (net book value of the land and buildings is £2.2bn). Putting all of this together suggests that investors are yet to recognise the true value of the businesses.

The information shown above is for illustrative purposes only and is not intended to be, and should not be interpreted as, recommendations or advice.

Past performance is not a guide to the future. The price of investments and the income from them may fall as well as rise and investors may not get back the full amount invested.

The new ‘in for frees’:

In addition to the stocks highlighted above, we now believe that there are other stocks that fulfil the ‘in for free’ criteria.

Royal Dutch Shell

Third Point, the US based activist fund manager, recently announced that that they had taken a significant position in Royal Dutch Shell in the belief that the entirety of the company’s stock market value is accounted for by what they termed its Energy Transition businesses (Integrated Gas, Marketing and Renewables) leaving its upstream, refining and chemicals businesses ‘in for free’. The former businesses generate EBITDA of $25bn which is valued on 10x would amount to the current enterprise value of $250bn. The latter three business units account for around 60% of the company’s profits and if accorded even a modest valuation (say 5x EBITDA) would crystallise upside of around 80% in the share price. Third Point are arguing for nothing short of a breakup of the company in order to realise this value and whilst they may or may not be successful, their action has demonstrated the potential inherent value that exists in the business.

Vodafone

A similar argument can be made for UK telecom operator Vodafone, although estimating what the constituent parts of Vodafone are worth is made considerably easier by the fact that certain parts of their business are listed (Vantage, Vodacom, Safaricom, Vodafone Idea and Indus Towers). Adjusting for these quoted assets, we can see how the stub is being valued and at today’s prices, it trades on around 4x EV/EBITDA and a 25% free cash flow yield. With the stakes in Vantage and Vodacom accounting for 60% of the equity value of Vodafone, there would appear to be a reasonable underpinning of the valuation of the residual business.

Conclusion

Rivian, a 12-year-old electric vehicle manufacturer with no revenue, listed on the US stock market last week and the shares doubled to the point that its market cap of $140bn made it the third most valuable carmaker in the world — just ahead of Volkswagen ($139bn), and in third place behind Toyota ($306bn) and Tesla ($1tn). To put the fact that it was valued more highly than Volkswagen into perspective, it is expected to produce c. 1000 cars this year versus 9.3m cars that Volkswagen produce.

Meanwhile, as we have tried to demonstrate above, there are still some very undervalued stocks available to investors including those that are so cheap that one division is worth more than the market cap of the entire group. In some cases, they are priced on mid double-digit free cash flow yields and high single digit dividend yields. But rather than take advantage of these bargains, investors are chasing story stocks like Rivian or ploughing their money into cryptocurrencies and non-fungible tokens. There are distinct echoes of 2000 in this behaviour and when the music stops, we know where we would rather be invested.

Past performance is not a guide to the future. The price of investments and the income from them may fall as well as rise and investors may not get back the full amount invested.

The information shown above is for illustrative purposes only and is not intended to be, and should not be interpreted as, recommendations or advice.

Unless otherwise stated, all opinions within this document are those of the RWC UK Value & Income team, as at 24th November 2021.